The modern credit card’s history stretches back to just after World War II, when the Charg-It card came out of Brooklyn, tied to a single bank.

Account holders could use the cards at a few local merchants, and the bank paid the merchants and billed the cardholders.

Then came the rise of bank-issued cards through the 1950s and 1960s. Debit cards sprang up in the 1960s.

But in 2024, closed-loop systems, embedded chips, a host of plastic cards in the wallet issued by several different banks, 16-digit numbers and CVVs to remember — well, it all seems so 20th century.

The movement toward digital channels, mobile devices, and the hypergrowth of advanced technologies such as artificial intelligence are changing the very ways in which cards are created, distributed, personalized and used.

The spate of announcements from Visa this week introducing seven new payment products contained an offering that helps to further what might be termed the “reimagination” of the card.

The “one card” concept and execution — via the Flexible Credential — enables a single, digitally-issued card to “toggle” between debit, credit, pay-over-time options and cryptocurrency. One card, connected to multiple banking accounts, eliminates the clutter for consumers that results from segmenting and juggling various banks’ credit and debit cards as they conduct their daily financial lives.

Separately, Visa also announced the ability to add credit and debit cards to mobile wallets through a tap, and to use cards to authenticate identity.

Cards are nearly ubiquitous. But how they’re used varies depending on where you look. PYMNTS Intelligence found that Generation Z consumers, for instance, are the most likely to use credit products or services to better manage their spending and cash flow, at 54% — the highest share across all age demographics. Millennials come second at nearly 52%. About 41% of older consumers do so.

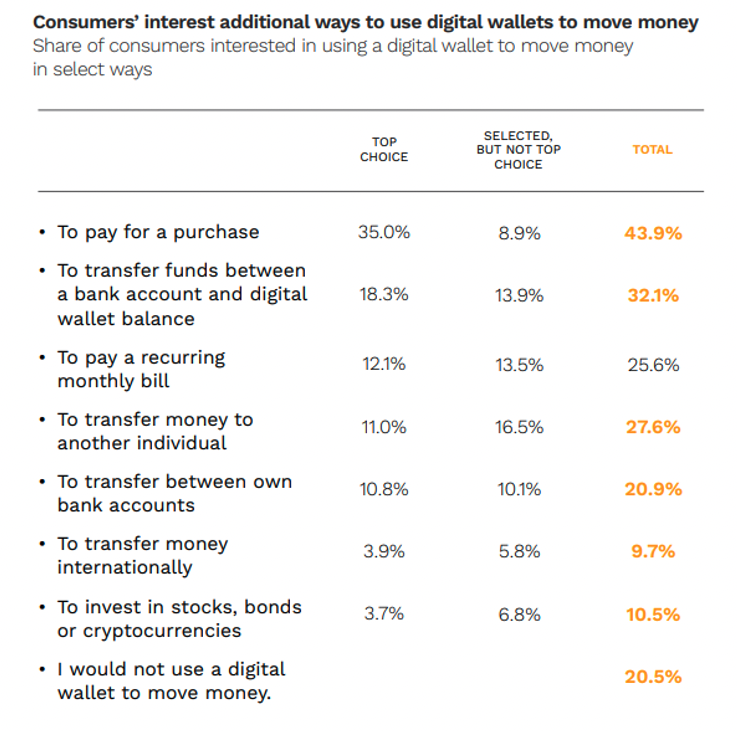

PYMNTS Intelligence data from the “Tracking the Digital Payments Takeover” series underscored the digital wallet as a hub for cards, a digital means of moving money between accounts and paying bills. About 80% of consumers said they would use a digital wallet for a variety of functions.

In recent months, there has been a shift in card spending (with momentum in debit), as using debit cards as the underlying digital wallet payment method when buying groceries has doubled in the last year. The data showed, for example, that debit cards garnered a 55% share of digital wallet spending for groceries. Older, high-income consumers used credit cards for 42% of retail purchases.

In recent months, there has been a shift in card spending (with momentum in debit), as using debit cards as the underlying digital wallet payment method when buying groceries has doubled in the last year. The data showed, for example, that debit cards garnered a 55% share of digital wallet spending for groceries. Older, high-income consumers used credit cards for 42% of retail purchases.

Cards issued by national banks still hold the majority among consumers, at 68% of cards issued. As PYMNTS found at the end of last year, two-thirds of consumers who have a primary bank account at a regional bank use a credit card issued by a national bank as their primary option.

Visa and PYMNTS Intelligence’s dive into click-and-mortar shopping found that digital experiences across channels and a plethora of payment options are among the features most in demand with consumers. AI-fueled banking and payment experiences, along with personalized, card-linked offers, can help push the use of cards digitally and with mobile devices in hand.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More